One of the biggest misconceptions in global investing is that everyone wants US Dollars and would abandon their local currency if they could.

It's an understandable assumption. The dollar is the world's reserve currency. Most global assets are priced in USD, and over the past several decades US markets have outperformed much of the world.

If you're building a financial product for users outside the United States, it's tempting to conclude that everyone should be converted into dollars as quickly as possible. Dollars become the canonical currency, while local currencies become little more than a funding rail.

Many international investing apps are built exactly this way.

But that's solving the wrong problem.

Most people don't wake up thinking about dollars. They think about pesos, naira, won, yen, euros, and pounds. That's the currency they earn, spend, budget, and save in.

What they actually want is access to the world's best assets without having to abandon the financial life they already have.

Of course, there are exceptions. In crisis economies like pre-Milei Argentina, Venezuela, or Turkey during periods of severe inflation, moving into dollars is often rational.

But for most of the world, something has changed.

Local Currencies Are Better Than They Were

For decades, the decision was simple: either hold local currency and lose purchasing power, or convert everything into dollars. Increasingly, that tradeoff no longer exists.

Inflation has moderated across much of the developing world, monetary policy has improved, and financial products have become dramatically better.

Instead of leaving money idle in a checking account, people can now earn competitive, market-rate yields directly from the fintech apps they use every day. Platforms like Nubank, Mercado Pago, and GCash have brought yield to tens of millions of users, making interest-bearing cash accounts a core part of the modern consumer banking experience.

In many markets, holding local currency while earning a competitive yield has become a perfectly rational decision.

Better local savings solved one problem: preserving wealth. They didn't solve the next: growing it.

As incomes continue to rise across emerging markets, people increasingly want more than a savings account. They want access to the world's best companies and investment opportunities.

The goal of global investing is simple: connect people to the world's best investment opportunities, regardless of where they live.

The best global investing products no longer force users to become dollar holders before they become investors.

Global Investing was Built for Americans

The first generation of global investing was built for Americans. That made sense. Most global assets settle in USD. Liquidity is deepest in USD. And American investors were the primary audience.

Companies like Interactive Brokers, Charles Schwab, and Fidelity built products for an American customer base. Thus, their platforms only supported USD.

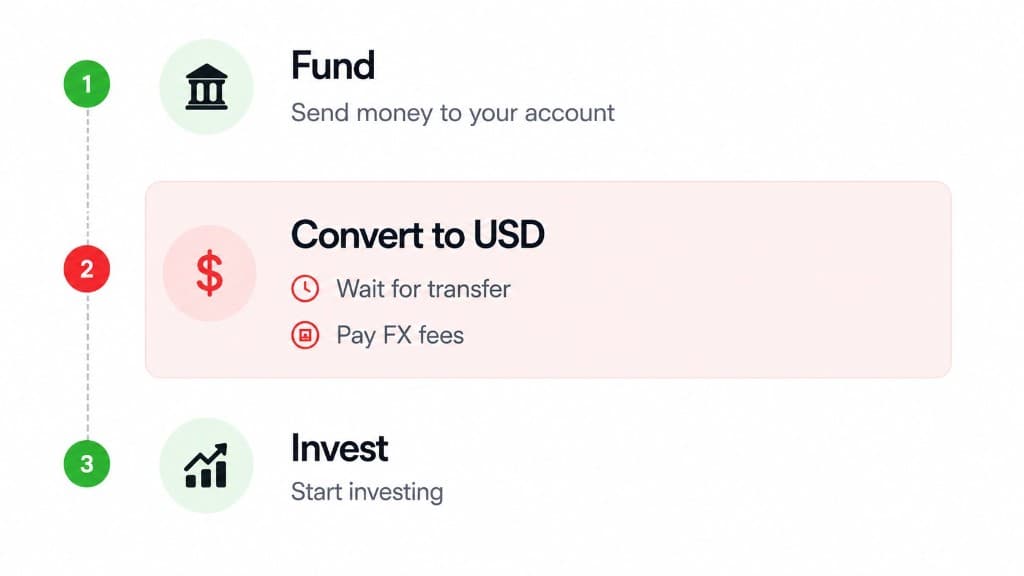

If someone outside the United States wanted to invest in a U.S. company, they first had to become a dollar customer. That meant finding a way to fund a USD brokerage account and later withdrawing in USD.

The burden of currency conversion was pushed onto the customer. Before they've even bought their first investment, users are expected to convert currencies, accept foreign exchange costs, and often wait longer for funding to complete.

Because getting USD required expensive international cross-currency transfers, not many international investors participated.

Some products bolt on local PSP funding flows to their USD-only exchange. This way local investors could easily fund through their local payment methods, but couldn't actually hold their local currency. This improved funding, but it didn't solve the underlying issue: users still had to convert into USD before they could invest.

More recently, products have emerged that solve this problem directly, broadening the pool of international investors.

The Modern Investing Experience Abstracts FX

The question isn't whether foreign exchange happens. The question is when.

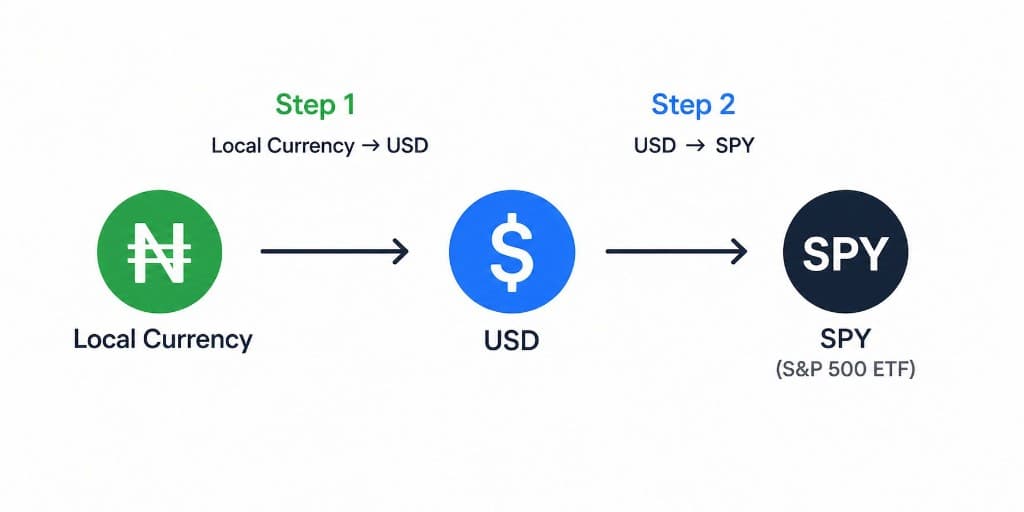

Almost all liquidity for an asset exists paired with USD, meaning first swapping from the local currency to USD and then from USD to the final destination asset must occur for best pricing.

Modern investing apps have abstracted the experience.

Users deposit and hold local currency into local cash accounts. When they buy a US stock, the required foreign exchange happens automatically just-in-time.

Foreign exchange only happens when it's actually needed, becoming infrastructure instead of workflow. The swap happens just in time, so users don't pay FX before funding their account or hold a currency they never intended to own.

Just-in-Time FX Is Becoming the Standard

Newer investing apps like Toss, Bamboo, Ajaib, and Arq were built around local funding from day one, and have had success scaling to tens of millions of users and billions in valuation.

These apps either partner with U.S. brokers or operate under their own licenses, enabling USD accounts, but have chosen to allow users to deposit via local payment methods at 1:1 because they know it creates a better user experience.

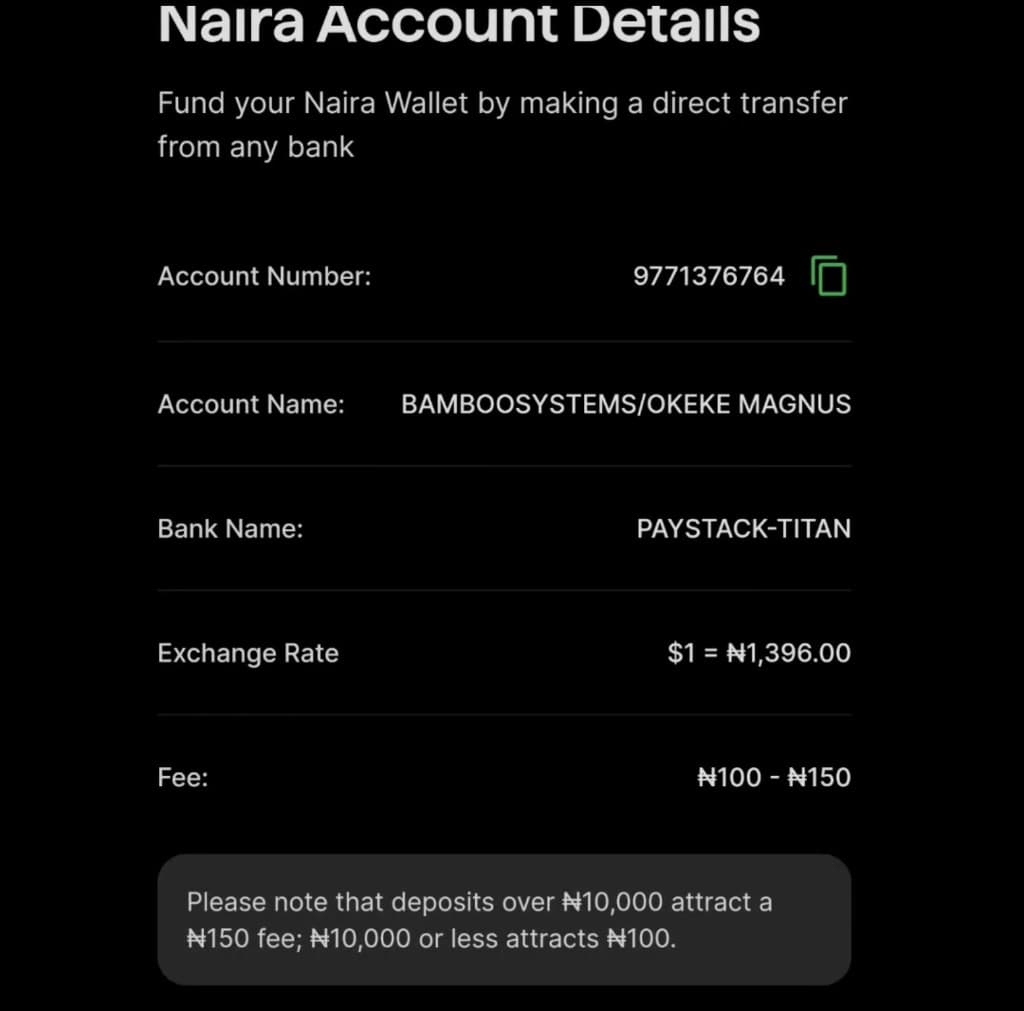

Bamboo illustrates the pattern well. Users fund in naira, can optionally purchase USD, and can buy U.S. stocks from either balance. USD becomes an option rather than a prerequisite.

Users can purchase USD if they'd like, but the default funding experience is all in local currency. When they want to buy a US-denominated asset like TSLA, the funds can pull from either the USD or local account.

As international apps are targeting the same users, they have followed suit. Established global brokerages are moving in the same direction.

eToro, for example, has been rolling out local currency accounts that let users deposit, hold, and withdraw funds in currencies like EUR, GBP, AUD, and DKK instead of forcing an immediate conversion into USD.

Users can then transfer funds into their USD investment account when they choose, or in some cases trade directly from their local currency account.

The implementation differs from product to product, but the direction is remarkably consistent:

Products are moving away from upfront FX and toward just-in-time FX.

Foreign exchange is becoming infrastructure rather than the first step in the customer journey.

Crypto Will Follow

Crypto apps today still largely leverage this USD-centric approach to funding and investing flows.

Despite offering region-agnostic assets from day one, most crypto products still revolve around U.S. dollar stablecoins and are funded either through expensive cards / sketchy P2P rails. That made sense when they were the only practical onchain currency.

As local stablecoins continue to emerge with retail-facing mint / burn capabilities and liquidity improves, crypto can follow the same path as traditional investing: users hold the currencies that make sense for their daily lives while foreign exchange happens only when transactions require it.

There is one important exception: Dollar-first experiences still make sense for users who already earn dollars.

We've seen the success of products targeting international freelancers, remote workers, and others receiving income from abroad via bank transfers or stablecoins. In these cases, the user naturally enters the product with USD, so a dollar-centric experience is a perfectly reasonable design choice.

But that's fundamentally different from serving the broader population, whose salaries, savings, and spending all begin in local currency. Products built around international freelancers are serving a valuable, but inherently narrower, segment.

The much larger opportunity is the billions of people whose financial lives still begin and end in local currency.

The Future Is Intent-First

The first generation of global investing exported American brokerage infrastructure to the rest of the world.

The next generation is exporting access, not infrastructure.

Users shouldn't have to think about settlement currencies, correspondent banking, or foreign exchange. They should simply decide what they want to own. Everything else should happen automatically.

Foreign exchange isn't disappearing. It's disappearing from the user experience. The product should optimize for the user's intent, not the underlying settlement infrastructure.

The future isn't USD-first.

It's intent-first.

Ready to invest intent-first?

Deposit in your local currency and access global markets at getgrowapp.co/join.

Join the public beta