There has been a lot of discussion about which tokenized equity issuer offers better pricing. The reality is that the answer depends less on the issuer and more on how the trade is executed.

To understand why, you first need to understand the two ways tokenized equities are traded today. Tokenized equities are executed using two fundamentally different models: onchain liquidity and RFQ-enabled intent networks.

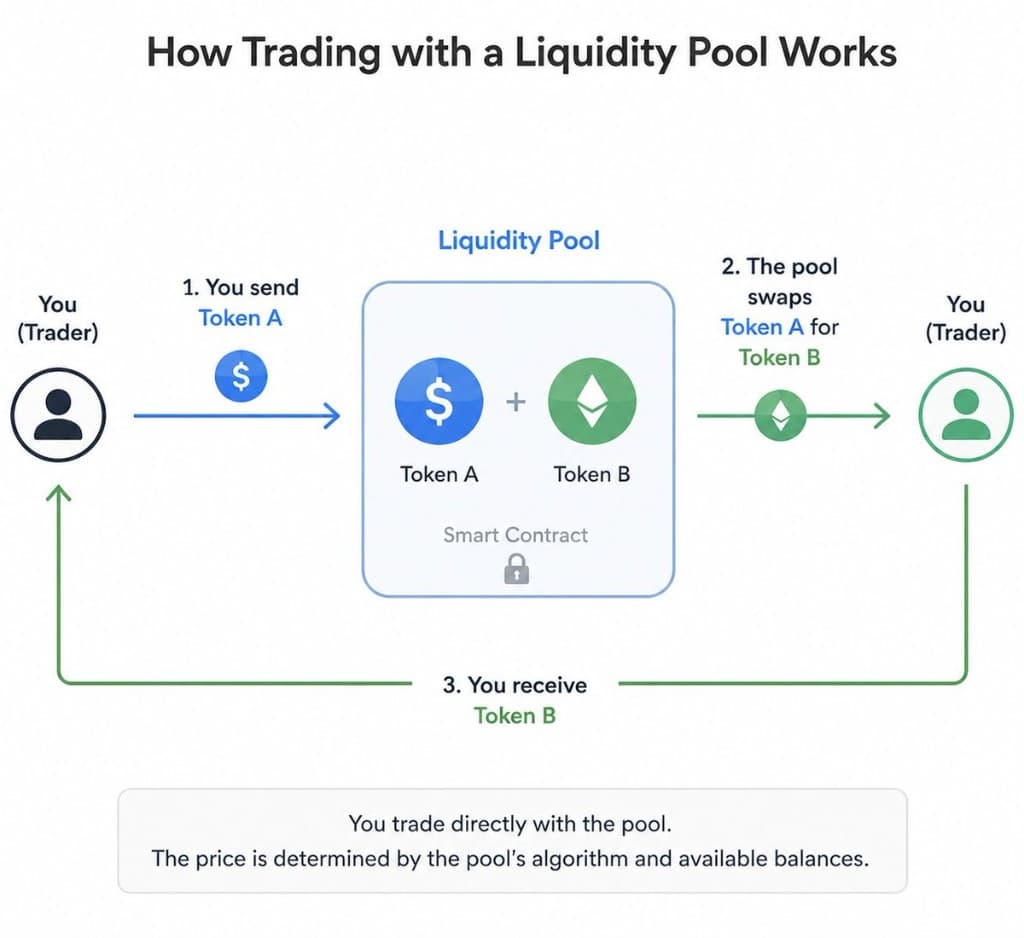

Onchain Liquidity

Assets have traditionally been traded in crypto using liquidity pools. For any two assets being traded, there's a pool onchain containing both tokens called a liquidity pool. Liquidity pools hold reserves of two assets. The relative amounts of each asset determine the quoted price.

If a user has Token A, and wants Token B they could deposit 10 units of Token A in the pool, and get out however many units of Token B is equivalent to the 10 units of Token A at that point.

When they deposit into the pool, the user changes the ratio of Token B to Token A, therefore changing the implied price. If the pool only has a small amount of liquidity and you try to swap a lot, you will move the price more and get less amount out. The difference between the reference price of Token A to Token B and the pricing a user gets is known as slippage. Therefore, if a token wants to have good pricing, you need a lot of liquidity.

The Catch — High Cost of Liquidity

Liquidity doesn't appear for free. Market makers and liquidity providers lock up capital in pools and expect to be compensated for doing so.

They earn trading fees whenever users swap through the pool, but they also take on costs. Their capital could be deployed elsewhere, and if the relative prices of the two assets change, they may incur impermanent loss. As a result, liquidity providers only supply capital where the expected returns justify the risk.

For most tokenized equities, organic trading volume isn't high enough yet to support the amount of liquidity needed for tight execution. To solve this, issuers often subsidize liquidity by paying market makers to seed pools.

The challenge is that these costs scale on a per-asset basis. Supporting deep liquidity for hundreds of tokenized equities quickly becomes prohibitively expensive.

As a result, only a small number of tokenized equities have meaningful onchain liquidity today, while the vast majority of assets are traded through RFQ-enabled intent networks.

RFQ-Enabled Intent Networks

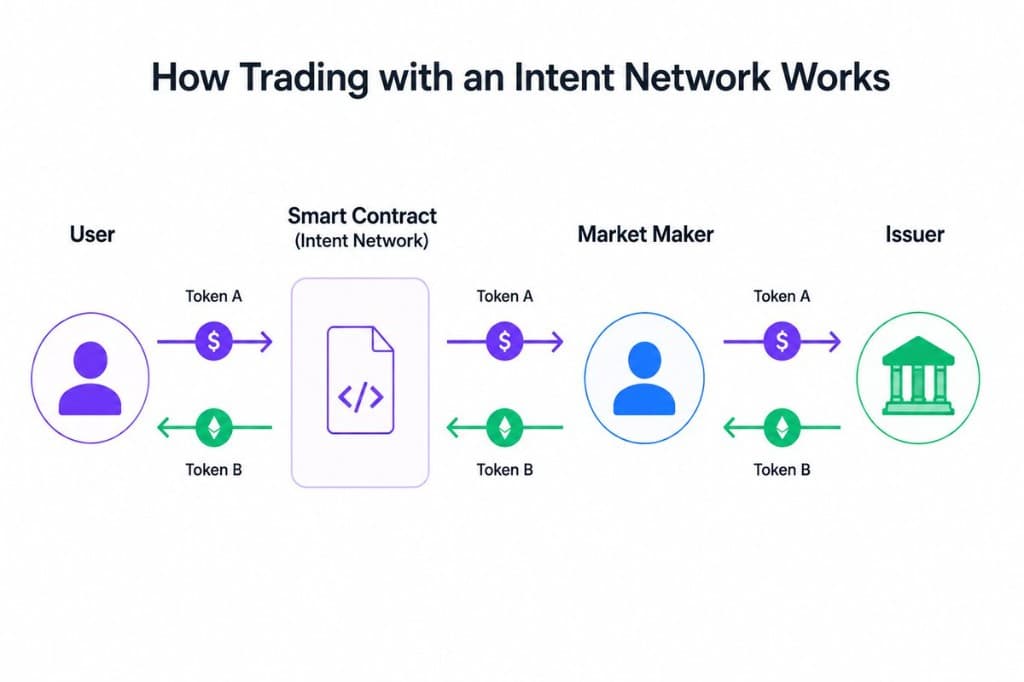

An alternative approach is to execute trades through RFQ (Request for Quote) intent networks rather than onchain liquidity pools.

Instead of swapping against liquidity already sitting onchain, a user broadcasts the trade they want to make. Multiple market makers compete to provide a quote, and the user selects the best one.

Where do those market makers get the tokenized equities to fill the orders?

Rather than buying from an onchain liquidity pool, they can mint and redeem directly with the issuer through an API. Because minting and redeeming typically requires KYC and KYB, users never interact with the issuer directly. Instead, market makers handle that relationship and provide liquidity to users through the intent network.

Once a quote is accepted, the trade settles atomically through a smart contract. The user deposits their assets into escrow, the market maker does the same, and the transaction only completes if both sides fulfill their obligations. This removes counterparty risk while allowing users to trade without relying on deep onchain liquidity.

As a result, execution quality is driven primarily by the fees charged by the issuer, market maker, and protocol, along with liquidity in the underlying offchain market, rather than by the amount of liquidity available in an onchain pool.

Intent networks make it practical to support a much broader universe of assets. Unlike onchain liquidity, each additional tokenized equity does not require its own liquidity pool. As a result, while onchain liquidity exists for only a handful of the most actively traded equities, the vast majority of tokenized equities today trade almost exclusively through intent networks.

The Catch — Market Closures

This model works well while the underlying market is open. During market hours, market makers can continuously mint and redeem with the issuer, allowing them to hedge their positions and keep quoted prices tightly aligned with the underlying equity.

Once the underlying market closes, that hedge disappears. Market makers can no longer immediately offset their exposure by trading the underlying stock, making it significantly riskier to quote prices. Historically, many intent networks simply stopped offering quotes outside market hours, making assets that relied exclusively on RFQ execution temporarily untradeable.

Recently, some issuers have introduced 24/7 mint and redeem APIs, making it easier for market makers to continue providing liquidity even when traditional markets are closed. While there is still no authoritative market price overnight or on weekends, market makers can reference other sources of price discovery—such as perpetual futures, related assets, and onchain markets—to estimate fair value. Because this introduces additional risk, quoted spreads may widen during these periods to compensate market makers for holding inventory.

What Model Gives the Best Execution?

There are important nuances to both models, but the following is generally true:

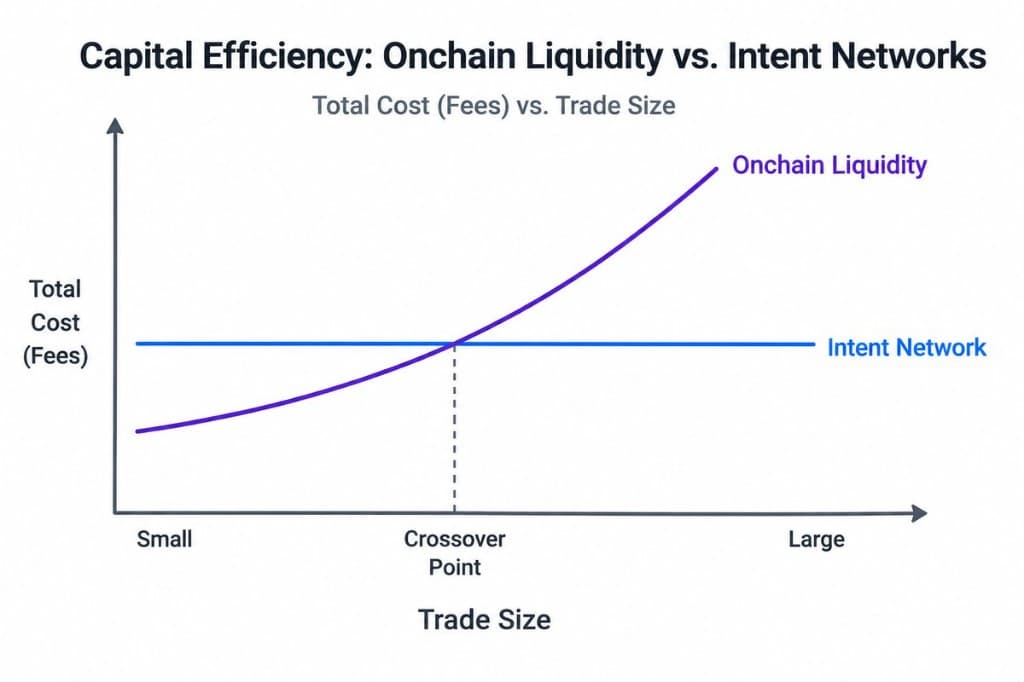

- For onchain liquidity, execution quality is primarily determined by the size of the trade relative to the available liquidity. As trade size increases, slippage becomes the dominant cost.

- For intent networks, execution is primarily determined by the fees charged by the issuer, market maker, and settlement protocol. Because liquidity in the underlying equity markets is extremely deep for most public stocks, it is rarely the limiting factor.

Smaller trades often achieve better execution through onchain liquidity, while larger trades often execute more efficiently through intent networks.

Which Issuers Give Better Pricing?

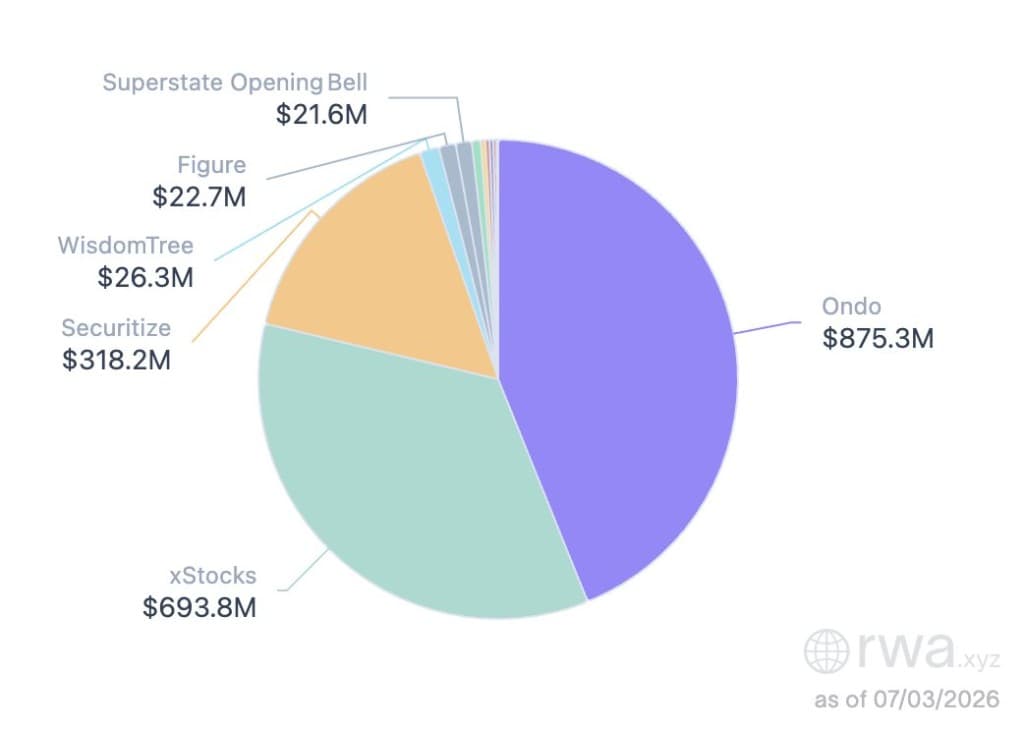

Currently, the two largest tokenized asset issuers by a wide margin are Ondo Finance and xStocks, accounting for 80%+ of tokenized stock volume according to RWA.xyz.

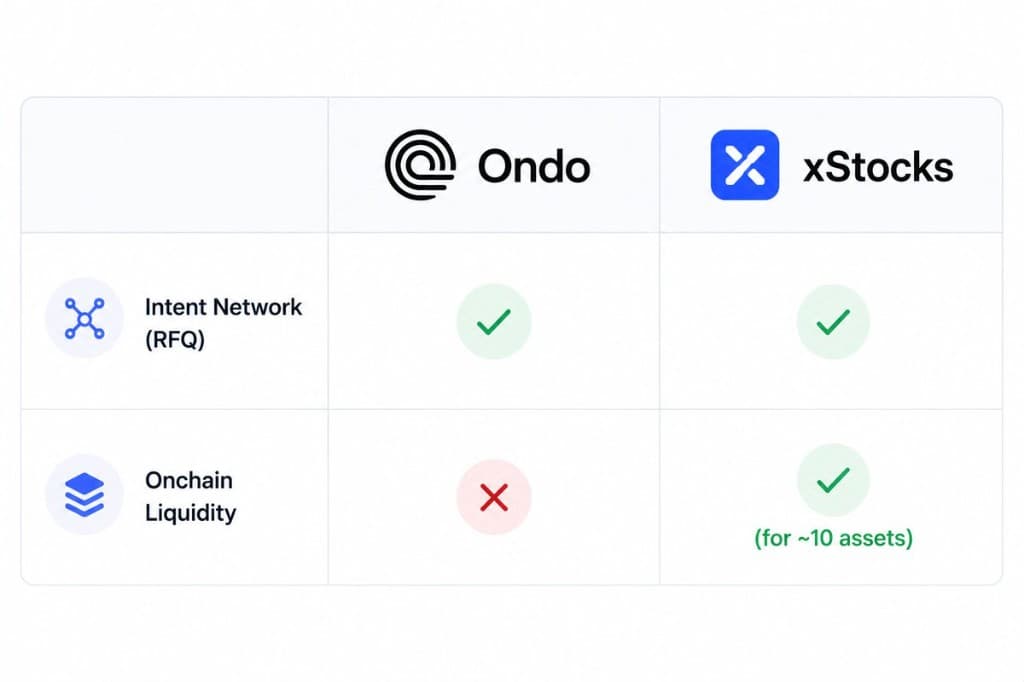

While both providers have claimed to offer the best execution through public posts, the reality is more nuanced. xStocks supports both RFQ-based execution and meaningful onchain liquidity for roughly ten of its most actively traded assets. Ondo currently relies exclusively on RFQ-based execution.

That alone doesn't determine which provider offers better pricing. The economics of minting and redeeming, issuer fees, market maker competition, and the specific implementation of each intent network all influence execution quality.

An analysis was run to validate the thesis among the two leading tokenized equity issuers. The following six assets' trade executions were compared across providers. They were chosen because they are shared between the two providers and have the most volume onchain (SPY, QQQ, CRCL, NVDA, TSLA, and GOOGL).

The results generally followed the dynamics discussed above.

Comparing the average percent difference in prices per venue across their flagship swapping paths:

- At smaller trade sizes, xStocks outperforms, largely due to swaps being routed through its onchain liquidity.

- At larger trade sizes, Ondo outperforms, largely due to better efficiencies in its intent network RFQ system compared to xStocks.

- In general, during market hours the spread between the two at amounts less than $100k are usually less than 0.1%, so whichever provider has superior pricing may not matter much when looking for the best returns.

- When the market is closed though, differences are much larger.

What Happens When the Market Is Closed?

Much of the trading volume in tokenized equities occurs outside traditional U.S. market hours. According to xStocks, approximately 45% of their trading volume takes place when the underlying equity market is closed.

This creates a different dynamic and one that allows for a more pure comparison.

During market hours, xStocks can route trades through both its onchain liquidity pools and RFQ-enabled intent network. When the market closes, however, RFQ execution is currently unavailable on xStocks, leaving onchain liquidity as the primary execution venue. Ondo, on the other hand, recently introduced 24/7 mint and redeem capabilities on the same six assets (SPY, QQQ, CRCL, NVDA, TSLA, and GOOGL), allowing market makers to continue providing RFQ quotes outside market hours.

This creates a clean comparison between the two execution models: xStocks' onchain liquidity versus Ondo's RFQ-enabled intent network.

The results support the theory discussed earlier even more dramatically than during trading hours, as there is no xStocks RFQ-enabled intent network which is more competitive at higher prices.

For smaller trades, xStocks' onchain liquidity generally provided better execution. As trade sizes increased, Ondo's RFQ-based execution typically became more competitive, with lower execution costs on larger orders.

At $42k, the average difference in price between the two methods across the six assets is 0. At ~$100k, the difference starts to become greater than 0.5%, and at $250k the difference balloons to almost 2% in Ondo's favor—the RFQ-enabled intent network.

The differences between the two issuers are far greater when the market is closed than when the market is open. This is because there is no way to mint and redeem from xStocks overnight, and Ondo must increase spreads to account for increased difficulty of hedging.

When a pure comparison can be done, the effect is even larger. For all sampled assets, the onchain liquidity route was better at lower trade amounts and the intent network better at higher trade amounts.

How Costs Scale

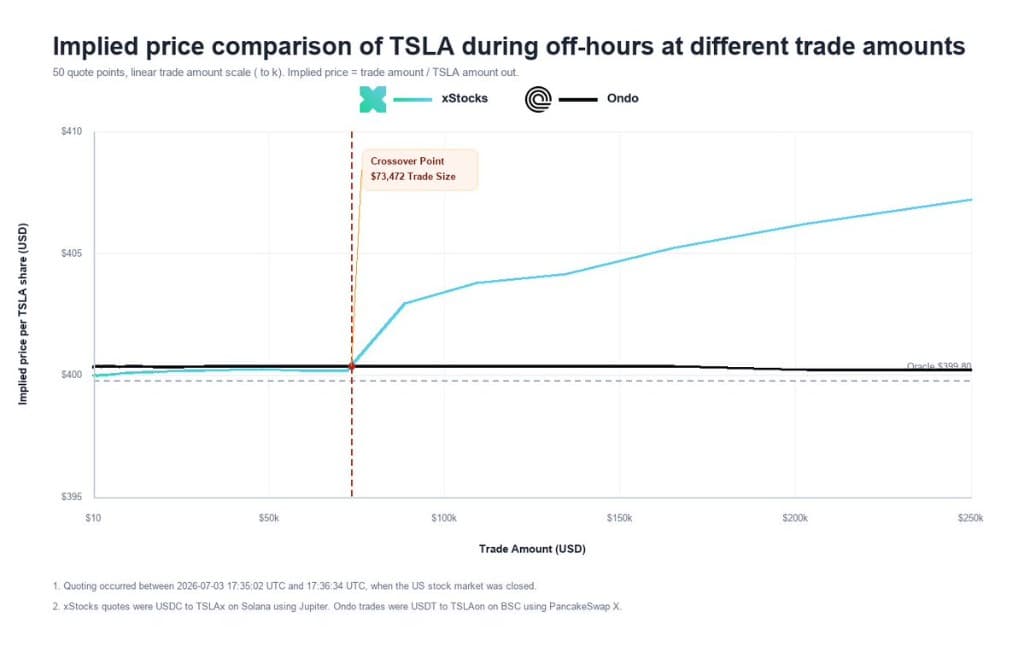

Zooming into TSLA specifically, you can see how the quotes almost perfectly mirror the simple execution price comparison diagram from earlier.

For onchain liquidity, execution costs increase non-linearly as trade size grows. Larger trades consume a greater percentage of the available liquidity, causing slippage to accelerate. As a result, doubling the trade size typically results in more than double the execution cost.

RFQ-enabled intent networks behave differently. Because market makers source liquidity from deep offchain markets rather than a fixed onchain pool, liquidity is rarely the primary constraint. Instead, execution costs are largely driven by issuer fees, market maker spreads, and settlement costs, which are often priced as a percent of volume, causing execution costs to scale approximately linearly with trade size.

This difference in cost curves explains why onchain liquidity often produces better pricing for smaller trades, while RFQ-enabled intent networks become increasingly competitive as trade sizes grow.

So What?

The data suggests there isn't a single tokenized equity issuer or execution model that consistently offers the best pricing. Execution quality depends on the asset being traded, the size of the order, market conditions, and how each issuer has implemented its infrastructure.

For most retail investors, price differences between issuers and trading venues are currently small. Saving a few tenths of a percentage point on execution is unlikely to have a meaningful impact on long-term returns, and factors such as supported assets, trading hours, custody model, and issuer risk may ultimately matter more.

For institutions and larger traders, however, execution costs can become material. As order sizes grow, intelligently routing trades through the most efficient execution venue can result in meaningful savings.

Different models have different strengths, and the best outcome increasingly comes from routing each trade through the venue that offers the best execution for that specific trade.

That's the approach we've taken at Grow. We integrate multiple leading tokenized asset issuers and route trades across multiple execution venues, including decentralized exchanges and intent networks. This helps users receive the best available execution.

We've also done the work of integrating and routing 20+ local stablecoins so you can deposit and withdraw via fiat cheaply and trade in the assets you use every day.

Learn more about Grow

Global markets, local currencies, and smart execution routing — at getgrowapp.co.

Get started